2023 Seed Stage Retrospective

A look back on crypto seed investments made in 2023.

Introduction

For the past two years, we’ve published our Seed Stage Retrospective in order to benchmark how that investment vintage has performed. We started to do this analysis internally to surface trends that inform our investment decision process. We decided to start publishing the data externally because we believe that it can help inform a more productive deployment of capital in our industry.

With this 2023 report, we apply the same framework, updating every chart and datapoint and adding several new ones to provide a comprehensive view of the 2023 vintage. Our dataset comprises publicly announced 2023 seed & pre‑seed rounds. We segment by sector &ecosystem to gather insights into the relative health of each. Let’s dive in.

Executive Summary

2023 was a year of reckoning for crypto founders. Following the collapses of Terra and FTX, seed capital flows fell off a cliff, and the venture ecosystem spent much of the year recalibrating. Total seed and pre-seed funding dropped roughly 50% year-over-year, with 680 companies raising ~$2.5B, down from 1,200+ deals and $5B in 2022. Important to keep in mind that fundraising announcements typically lag the actual fundraise by 6 months, so what you are seeing is the fallout of the crypto market that started with the UST depeg in May 2022.

Key takeaways from the 2023 SeedVintage:

● There are 5 tokens with a current FDV over $1B from the year, less than 1% of funded companies.

● The amount of capital invested at seed did not correlate with better token outcomes.

● 25% of seed project teams raised follow-on capital, up from 12% in 2022, but overall teams are still in line with the prior year, given the sharp decline in seed rounds in 2023.

● Only 15% of teams have successfully launched a token after 2+ years of building.

● AI & DePIN emerged in 2023 as notable new sectors capturing ~$100M in funding and posting the highest follow-on rates amongst sectors.

● Following FTX, Solana ecosystem teams struggled to raise but had some of the highest follow-on rates and lowest failure rate amongst ecosystems.

● Exchange related funds (e.g. Yzi labs fka Binance labs) had the highest percentage of teams that were able to successfully launch tokens.

Methodology

This report is based on a combination of first-party data, supplemented by insights from Messari, Root Data, Crunchbase, and other sources. To evaluate the progress of the seed-stage market, we categorized each company by stage, including "Active No Product Shipped" and "No Longer Active," defined as projects that are still active on social w/o a product or have not posted on social in more than 3 months. Additional segmentation is done by ecosystem and sector. While we have made every effort to ensure data accuracy, we acknowledge that there may be errors due to the reliance on third-party data. In our graphs, we included only ecosystems with more than 10 teams that raised an initial round of funding.

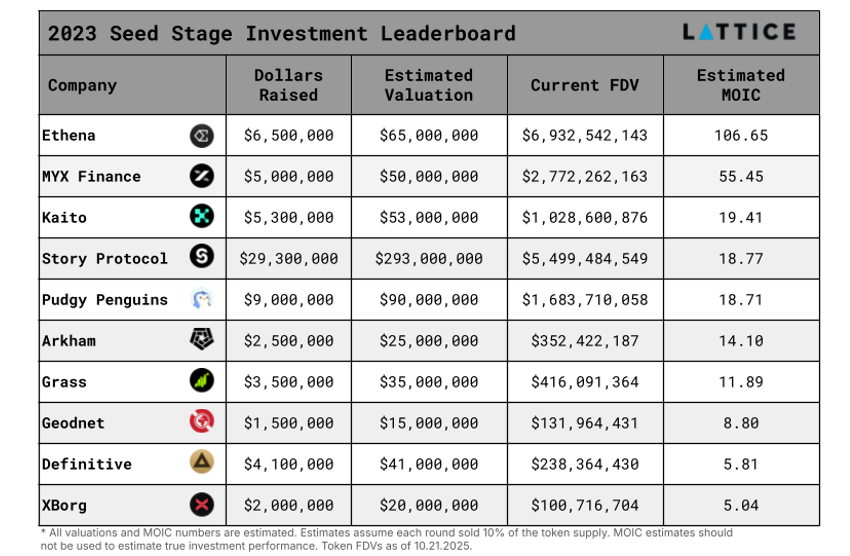

2023 Crypto Token Unicorns

- Ethena - $6.9B

- Story-$5.5B

- MYX Finance - $2.7B

- Pudgy Penguins - $1.6B

- Kaito - $1B

- *Two other major winners from the 2023 vintage; Hyperliquid’s DEX launched in 2023 though they never raised a VC round and it is rumored that Pump also raised a seed in 2023 though this was never publicly announced.

While hunting unicorns is important, what investors are ultimately looking for is the maximum multiple on invested capital (MOIC). This further illustrates the advantages of getting into those unicorn deals, as well as the ability to generate returns from mid-cap projects.

Seed Check Size Has Weak Predicitive Power on Token Valulation

Not surprisingly, there is a weak relationship to token valuation. Most projects, whether they raised $3M or $15M, cluster near low FDVs, while a few outliers account for nearly all of the upside, and those outliers (e.g. Grass) did not raise the largest rounds. The shallow trendline (R² ≈ 0.2) suggests that larger early checks do not necessarily lead to stronger token outcomes.

The State of Seed

Probably the single most important predictor of a project's success is the ability to ship product and ship fast. Since starting this analysis in 2021, we’ve seen a fairly consistent trend: with roughly 60-70% of companies shipping to mainnet or an equivalent, 15-20% shutting down, and the remaining companies either having been acquired or in a yet to go live state - the 2023 vintage is no different, and it remains consistent with startup failure rates outside of crypto

Another way to assess the ‘success’ of capital deployed is by examining the percentage of companies in the data set that are still operating. The expectation in venture is always that many of the companies invested in will eventually fail, but ideally, as many dollars as possible are still working at any given time. Thus, if we use dollars still at work as the primary metric to consider, roughly $0.92 of each dollar from the 2023 vintage is still on the table as we head into the last quarter of 2025. That’s pretty good and all the more impressive considering the number one subsector of 2023 was gaming, which you’d be hard pressed to realize is even a sector in crypto anymore with a clear lack of conversation and fundraise announcements.

Fundraising

While 2023 was a difficult fundraising environment at the seed stage, it actually provided a healthier follow on fundraising environment. 25% of 2023 seed teams have successfully raised follow-on rounds vs. the 12% we saw from the 2022 cohort.

Interestingly, this means that given the roughly 50% decline in seed stage startups, the number of Series A companies remained constant. This suggests that at least over the last few years crypto capital markets can only support roughly 150 Series A companies. Obviously, that can change as capital inflows slow or grow, and the extent to which generalist venture funds are willing to lead Series A rounds for crypto businesses.

Token Launches

The path to liquidity continues to be a challenge for crypto markets. In our first State of Seed report covering the 2021 cohort. 50% of that vintage launched a token within two years of raising a seed round. That percentage fell to 15% in 2022 and remained flat at 15% for2023. Given the 50% decline in seed rounds from 2022 to 2023, this translates to only 100 new ‘VC’ tokens launched from the 2023 vintage, compared to 180 for the 2022 vintage. This further demonstrates just how challenging the crypto VC market has been.

We believe there are several drivers behind this continued decline in new token launches. The first we talked about last year, which is the reliance on centralized exchanges and the associated costs, but the second reason is even more important and will likely have longer-term implications for token projects and venture investors.

Speculation on new tokens was, for a longtime, the speculative game for retail, but over the past several years, the diversity of ways to speculate in crypto has increased. In 2021, we saw the emergence of NFTs, but more recently, we’ve seen the rise of meme coins, perpetuals, and prediction markets as totally new speculative options for the crypto degen. Unless a team is generating revenue or fits well into a hot narrative, there has been a dearth of buyers for new tokens. We believe everyone waiting for a market-wide“alt season” is likely going to be waiting for a long time, due to the cumulative nature of liquidity and attention fragmentation across tokens. Given the relatively low ‘death rate’ of VC tokens, even in a muted market like 2023the number of tokens competing for a relatively static market of buyers increased dramatically.

Four Horsemen No More

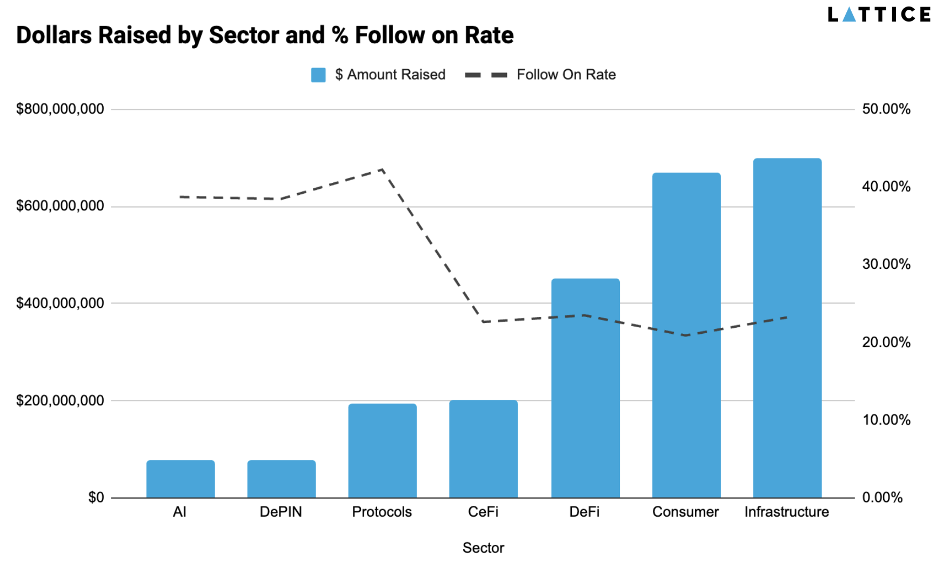

In our first two years of reports, our sector analysis comprised 4 broad sectors: DeFi, CeFi, Infrastructure, and Consumer. The maturation of the asset class has led to an expansion of broad sectors with the addition of DePIN & AI and our decision to break out protocols (L1s & L2s) from the infrastructure category (analytics, bridges, etc).

All sectors were down on a year-over-year basis, with consumer and infra continuing to dominate, and venture dollars were only beginning to flow into emerging sectors, DePIN & AI.

The 2023 seed cohort had meaningful divergences across sectors in both execution speed and survivorship. The two standouts come from 2023’s sectors: DePIN & AI. DePIN projects have shipped at a high rate, with over 90% delivering a live product within two years.

On the flip side of that is AI, with less than ½ of teams delivering a product to date. While this may present as bearish for the AI sector, digging into the underlying projects you’ll find a large percentage of AI companies are working on deeper technical problems that will likely take longer timeframes to develop.

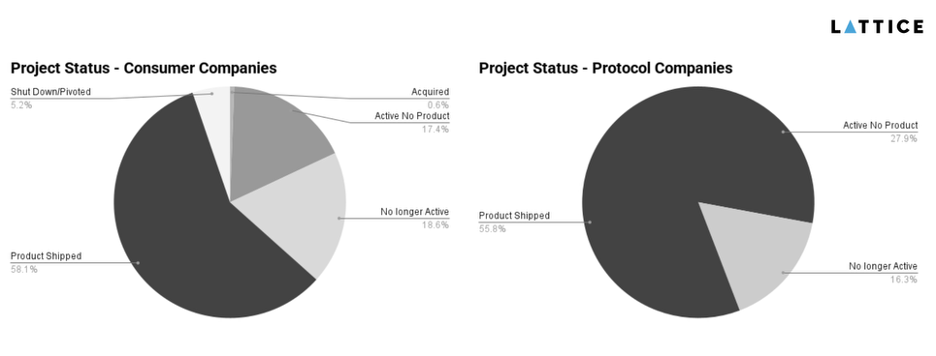

Consumer and protocol layer projects have seen the least success in terms of shipping product. On the consumer side, fewer than 60% of projects managed to deliver a product, and nearly one in five shutdown altogether. That reflects a reality where successful non-speculative crypto consumer apps are still largely non-existent. 2022/2023 had been a period of expected consumer oriented adoption on the heels of the NFT bull market - many of those projects never materialized in a meaningful way. In addition, the 2023 cohort included more than 70 gaming projects, which have seen minimal user adoption.

At the protocol layer, the challenges stem from the opposite problem: long build cycles and an increasingly crowded base-layer landscape. More than a quarter of protocol projects are still “active with no product,” and another~16% have already gone inactive, underscoring how hard it is to bootstrap new ecosystems in today’s environment. With L2s like Base maturing and Solana’s resurgence post FTX, new protocols from the 2023 vintage have struggled to attract developer mindshare or raise the resources necessary to reach mainnet beyond massive token incentives, which have mostly failed to attract sticky users and developers.

Unlike DePIN & AI, the story with this final grouping isn’t about dramatic divergence but about consistency. DeFi, CeFi, and Infrastructure all show product launch rates in the 65–72% range, with inactivity clustering in a fairly narrow band of 15–19%.That steadiness reflects the fact that these sectors remain the “core” categories of crypto: they’re closest to the financial rails and technical backbone of the ecosystem, attracting many of the most experienced teams that operate in more well-defined markets with clear PMF. Unlike consumer or protocol layer startups, they don’t have to invent entirely new user behaviors or ecosystems from scratch.

The Aftermath of FTX

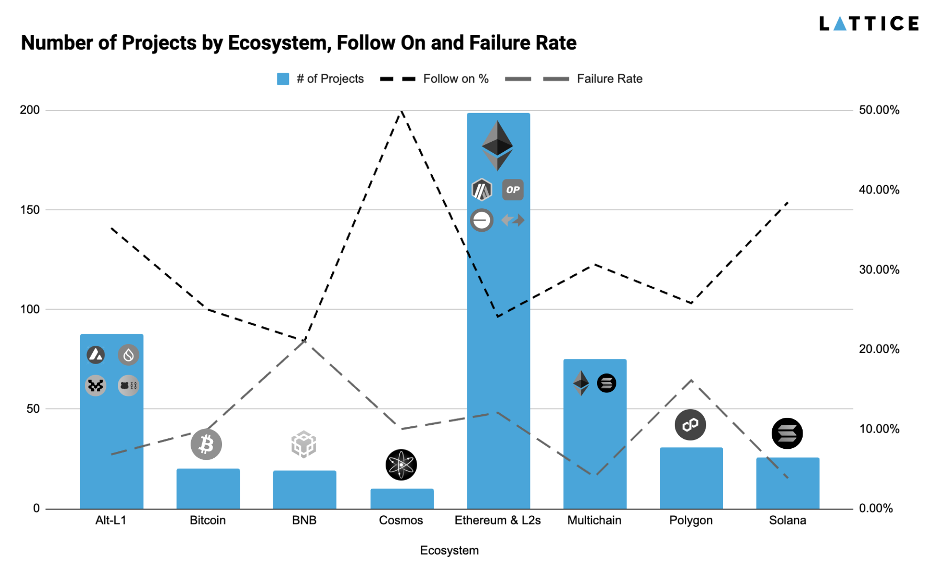

Digging into the ecosystem-level data is where things start to get really interesting. First, let us take a trip back to 2023.FTX has just collapsed, and the price of SOL has fallen from an ATH of $250 to less than $10. To say the sentiment around the Solana ecosystem was negative is an understatement, and the proof is in the decline in the number of teams and the amount of funding at the seed stage, as well as the dominance of the broader Ethereum ecosystem in that year.

Ethereum and its L2s accounted for the overwhelming majority of new seed projects. To be expected, follow-on rates for Ethereum-based projects clustered around the middle of the pack, and failure rates were about average. The abundance of teams competing for capital and attention may have diluted the cohort’s overall success.

Solana, by contrast, tells a different story. A smaller number of projects managed to raise that year, but those that did went on to post some of the highest follow-on rates and lowest failure rates in the dataset. The data reflects a powerful survivor bias, only the most dedicated founders and highest conviction investors stuck with Solana post FTX. Two years later, those contrarian bets look prescient. After the ecosystem rebounded sharply, the 2023 vintage of Solana projects stands out as one of the highest-quality subsets in the entire seed landscape.

2023 Venture Fund Performance

New in this year’s version of our retrospective is an analysis of the venture funds operating in the space and how each fared in 2023. It’s important to keep in mind that, at the end of the day, the only thing that really matters for venture funds is generating returns for investors, but without access to certain levels of data and only two years of look-through post-investment, we are limited in what we can share. With that said, there are some leading indicators we can look at with publicly available data to get a sense for how the venture fund ecosystem fared during the bear market period of 2023 beyond the three big winners mentioned above.

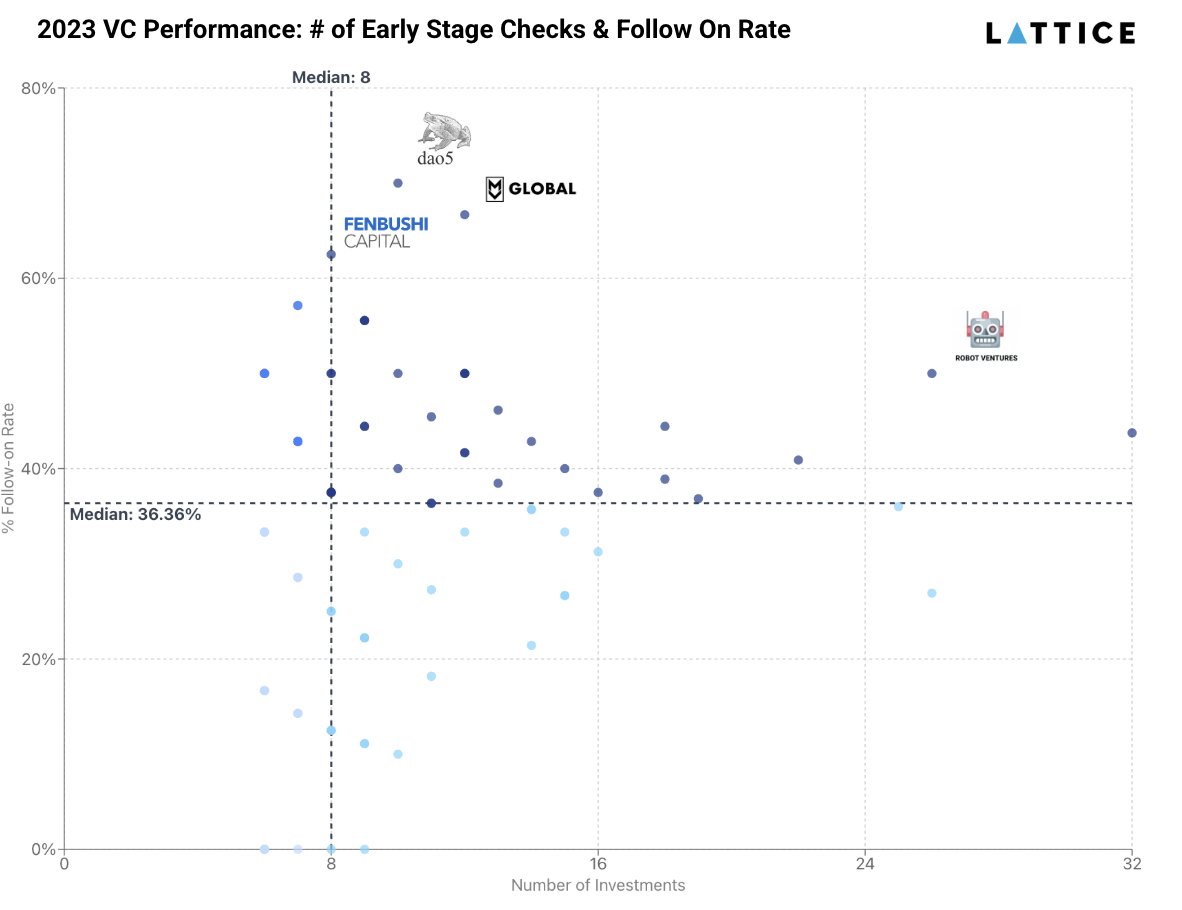

Follow-On Rates

Given that this report focuses on seed & pre-seed companies, a fund having a high hit rate for follow on investments is a pretty good indicator that they are on the right track. The funds clustered on the left side of the chart are taking a more concentrated approach (making fewer than ~10 investments) and show the widest spread in outcomes. Some concentrated funds outperformed the average, with follow-on rates exceeding 50–60%. Notable call-outs here include DAO5, MV Global, and Fenbushi Capital, with their investments receiving follow-ons at or above 60%

As we move along the X axis, funds with larger portfolios of 15–30+ companies, the variance narrows, regressing toward the mean, with follow-on rates converging around 30-40%. The biggest outlier moving further out is Robot Ventures. Tarun & Robert’s deep founder network is not only getting them access to a lot of deals, but they are better than average at picking them with a 50% hit rate across 25 investments that year -impressive indeed.

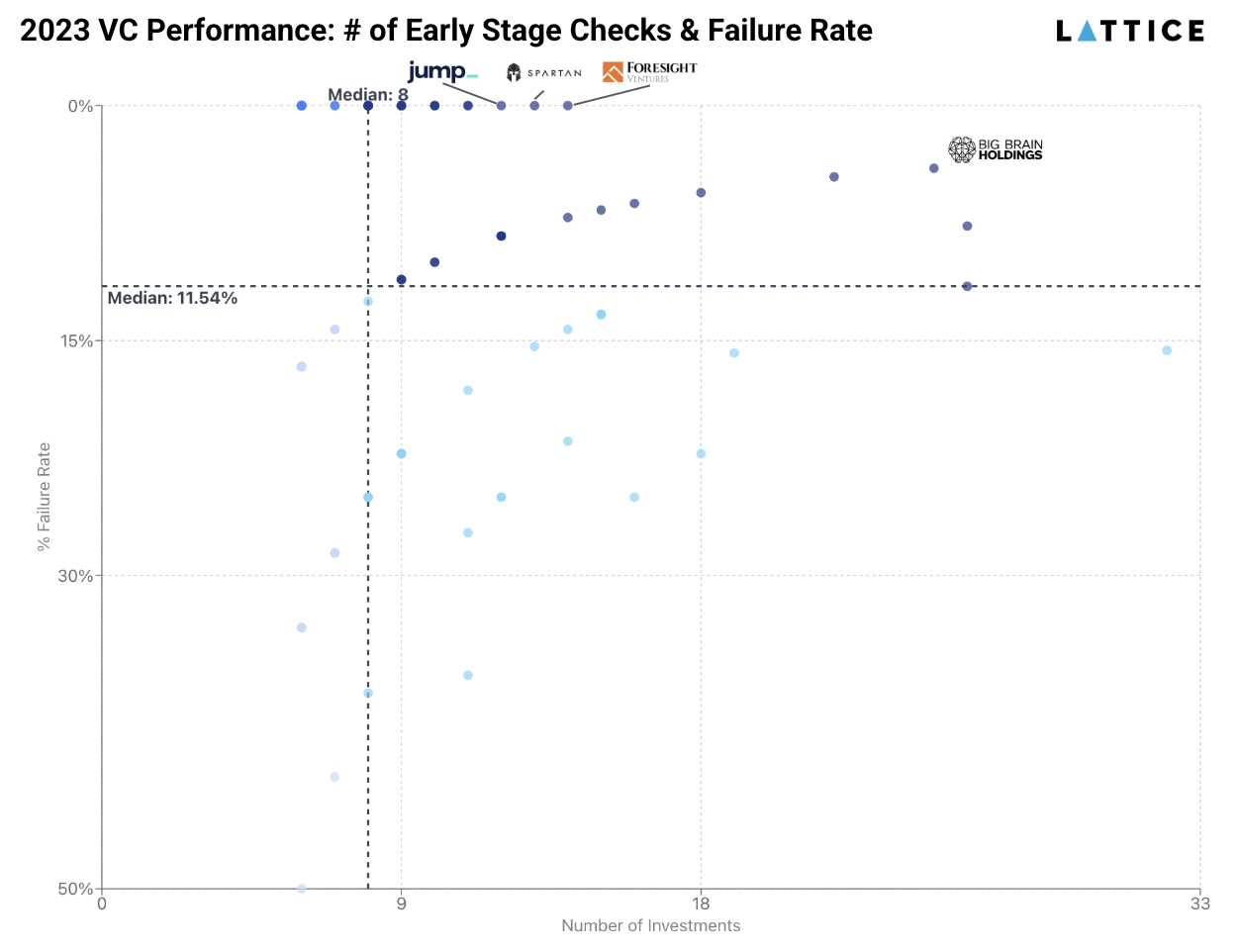

Failure Rates

The risk of a failed investment is just part of the job, but it is still interesting to look at the trends across funds when it comes to what percentage of investments are no longer operational after two years. Funds with small portfolios(5–10 deals) exhibit the widest range of failure rates; some are experiencing 40–50% of their companies going inactive, while others manage near-zero attrition. Foresight, Spartan, Jump, Maven11, and Lemnis still have all their chips on the table with more than 10 seed investments in 2023, and all are still operating.

Token Launches

We operate in a token world, and while it’s becoming increasingly challenging to bring tokens to market, it's clear that some funds are having more success identifying and investing in projects that will launch tokens. While this one doesn’t shock us, it does give credence to getting one of the leading Asian exchanges on your cap table with venture arms of asian exchanges Binance (YziLabs), KuCoin, and OKX holding three out of the top four positions on the percentage of investments that are able to launch a token, with Inception Capital being the only non exchange affiliated venture firm with a token launch rate above50%. US exchanges, on the other hand, are likely not going to help you with Coinbase Ventures and Kraken Ventures sitting at 22% and 0% respectively.

Conclusion

2023 was a challenging year in crypto that has generated several outsized winners with Ethena being the crown jewel of the class. The 2023 story continues to unfold with more than 120 teams that raised follow on rounds yet to launch tokens, including notable projects like Monad and other successful companies which may never launch a token e.g. Felix. We fully expect more value to be realized as these businesses grow and mature and look forward to next year’s publication, where we’ll follow up with this year’s class along with the class of 2024. The lesson we’ve taken from each years analysis has been to tread carefully when investing in the current in market trend. Given Polymarket and Kalshi’s recent fundraises, the environment for prediction market investing feels strikingly reminiscent of prior market trends like NFTs with OpenSea’s $13B valuation or Axie Infinity. While we believe prediction markets likely offer better staying power, we are cautious when looking at new deals in the sector. Beyond that, stablecoins, payment related business, and yield products continue to be where most action is at the seed stage and while historic trends have shown to look elsewhere, we believe for one of the first times in crypto you have clear product to market fit and we expect there to continue to be positive outcomes from these sectors and are potentially under-hyped if anything.

Don’t Miss Our Latest News

Subscribe to our newsletter and get all the news from Lattice.

No spam, we promise.

.svg)

Your message was sent sucessfuly.

.png)

.png)